Footy Tips

Footy Tips

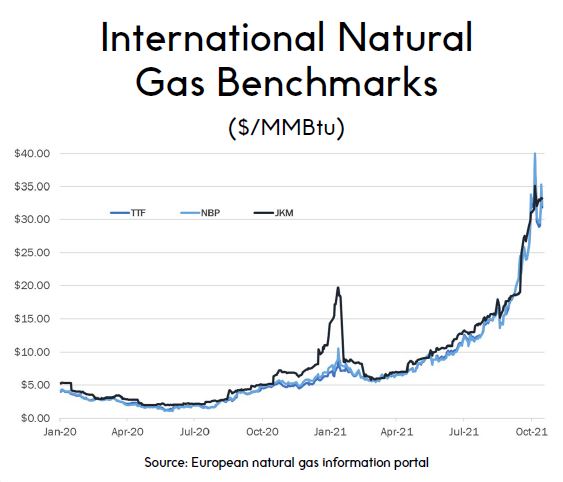

Supply Chain challenges throws cloud over inventory availability. The worsening global supply chain situation continues to drive concern over the access to product in 2022. Paul Zahra, CEO of Australian Retailers Association commented recently that the supply chain woes will likely continue until 2023. Consumers will likely be paying higher prices for goods in the new year.” Product availability may well be an issue in 2022 and this is intrinsically linked to product manufacturers price expectations. Predicting when energy prices will subside is difficult due to political gamesmanship going in Europe. As recently as November 16, 2021, the Guardian reported, Germany has suspended its approval process for the controversial Nord Stream 2 gas pipeline which would double its reliance on Russian gas following growing geopolitical pressure to scrap the project. Energy markets across Europe surged after the German energy regulator suspended its certification process, in a big setback to Kremlin-backed Gazprom’s plans to extend Russian gas dominance via a new pipeline across the Baltic Sea. UK gas prices for next month (Dec / Jan) surged 9.3% on Tuesday, while the Netherlands – which is one of the biggest gas markets in Europe – suffered an increase of 7.9%. Best guesstimate has this crisis not being resolved until after the European summer at the very earliest. As you can see from the graph Gas prices since Jan have increased by 600%.

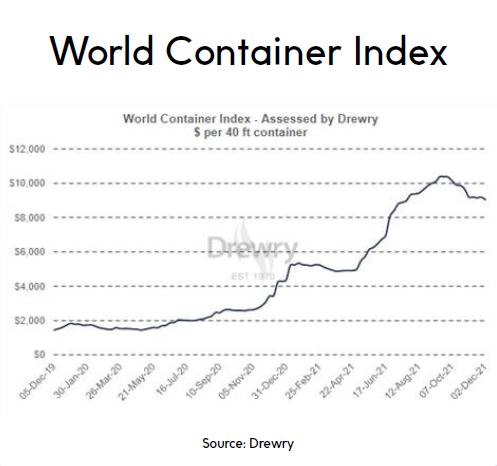

International Shipping Over the past 12 months, international shipping costs have increased from $2000 to $10,000 USD for a 40ft container. Freight Specialists continue to indicate that the worst is not over even with a slight downturn last month. These increased levels are expected to remain in place for most of 2022.

The factors driving this include:

• Continuing massive upswing in global commodity trading related to the bounce back from Covid lock-downs.

• Massive global container equipment imbalances and main port congestion adding to difficulty matching supply with demand.

• Increases to local landing charges.

The factors driving this include:

• Continuing massive upswing in global commodity trading related to the bounce back from Covid lock-downs.

• Massive global container equipment imbalances and main port congestion adding to difficulty matching supply with demand.

• Increases to local landing charges.

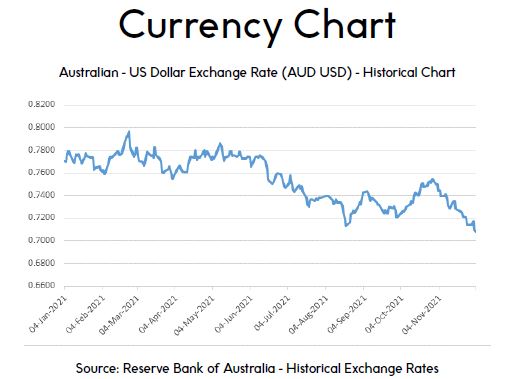

Hasn’t the exchange rate (AUD vs USD) mitigated some of these increases? Up until June 2021 yes. Since our October update the AUD vs USD exchange has further declined to $0.717 (at time of writing). tradingeconomics.com forecast the AUD to be trading at 0.69 and 0.68 by the end of 2022. If this is accurate, this means a 10% increase due to currency alone.

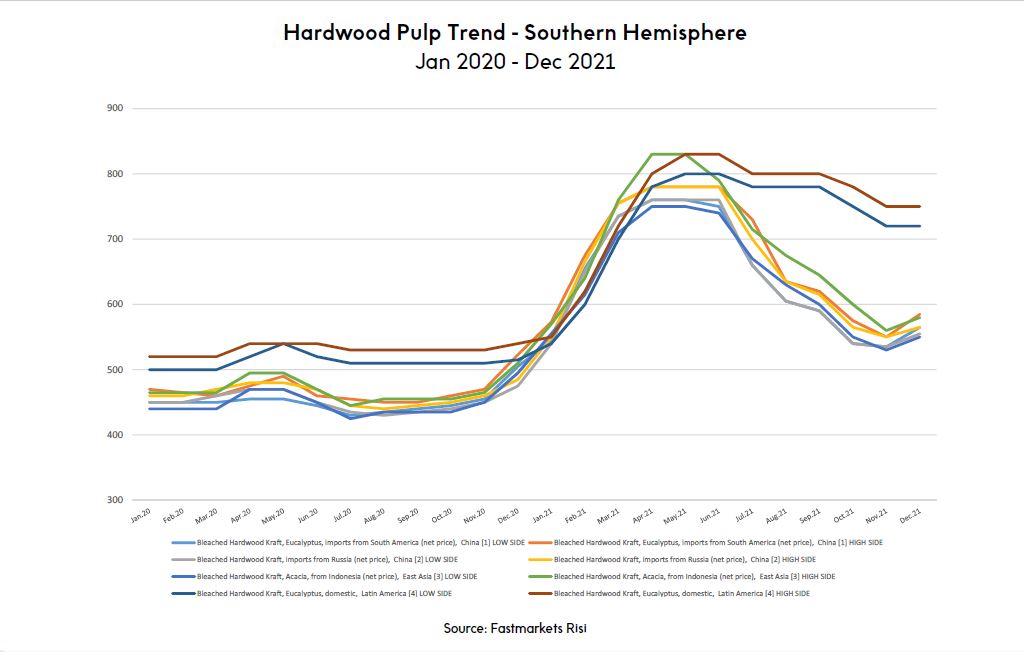

Pulp Pricing Further pressure on pulp pricing as a result of: • High demand for fibre based packaging due to the pandemic. • Strong demand from the building and textile industries as economies rebound from COVID. • Shift from plastic to fibre based packaging due to environmental concerns. • Increases in ocean freight to transport from pulp mill to paper mill. • Unsustainable low historic pricing from all pulp manufacturers globally. • The consolidation of major pulp producers controlling supply and demand. Although we are seeing a reduction in pulp prices, Pulp production is one of the most energy intensive industries. Recent energy increases continue to increase overall costs.

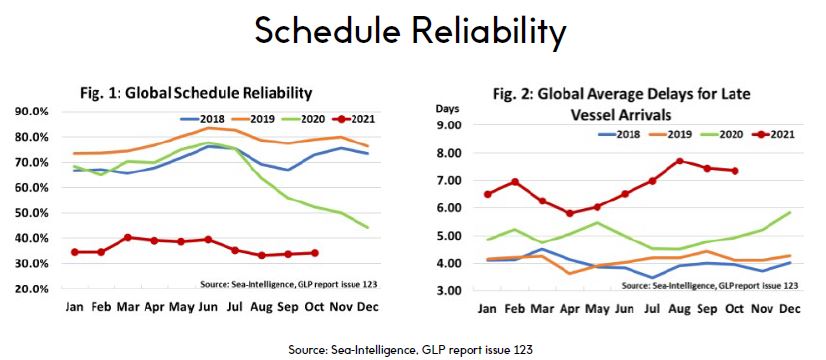

Along with this, schedule reliability is at its worst ever level as seen in the graphs below. This is due to a number of reasons including trans-shipment, port congestion and blank sailings (cancellations or skipping of schedule port stops).

• Schedule reliability is the measure of a shipping lines ability to deliver within specified dates (DIFOT).

Along with this, schedule reliability is at its worst ever level as seen in the graphs below. This is due to a number of reasons including trans-shipment, port congestion and blank sailings (cancellations or skipping of schedule port stops).

• Schedule reliability is the measure of a shipping lines ability to deliver within specified dates (DIFOT).

Other operating cost pressures include but are not limited to; pallets costs with Timber increasing by 34% in the past 12 months, fuel and a tightening labour market. These cost pressures are having an impact on day to day consumer goods for example, Canola Oil up 76% in last 12 months, Cotton up 56% up in last 12 months, Coffee beans up 118% in last 12 months.

Other operating cost pressures include but are not limited to; pallets costs with Timber increasing by 34% in the past 12 months, fuel and a tightening labour market. These cost pressures are having an impact on day to day consumer goods for example, Canola Oil up 76% in last 12 months, Cotton up 56% up in last 12 months, Coffee beans up 118% in last 12 months.

In Summary, there are six key factors that are impacting the global supply chain and putting upward pressure on pricing and availability; 1. Soaring Natural Gas prices in Europe that effect global manufacturers with increased costs. 2. Supply chain and logistics disruptions arising from the pandemic. 3. Massive spike in freight costs, especially to the ANZ region. 4. Capacity reduction by Paper mills globally rebalancing supply and demand. 5. Solid global demand as economies rebound from COVID. 6. Continuing decline in the Australian dollar against the USD. If you require any further information please contact your Ball & Doggett Sales Executive.